#64🚀 Who will lead the Magnetics Industry?

SuperPowers for Electrical Engineers 🦸🏻♂️🦸🏼♀️

👋 Hello, friends! Dr. Molina here 👨🔧

Welcome to Dr.Molina Newsletter, where I break down Magnetic design for you every week, in

4 minutesthe time needed.

Happy New Year to everyone. I wish all of you a happy 2023!

Today, I bring to you a thought, a parallelism between semiconductors and magnetics. I would love to listen your opinion after you read it.

During Christmas, I walked around Mediterranean beaches listening to podcasts and reading about the semiconductor industry.

Some of these podcasts revealed some information that surprised me.

Chips were trending because of the global Shortage, but I’m not going to talk about the shortage. The shortage affects mainly to microprocessors, memories, and logic IC.

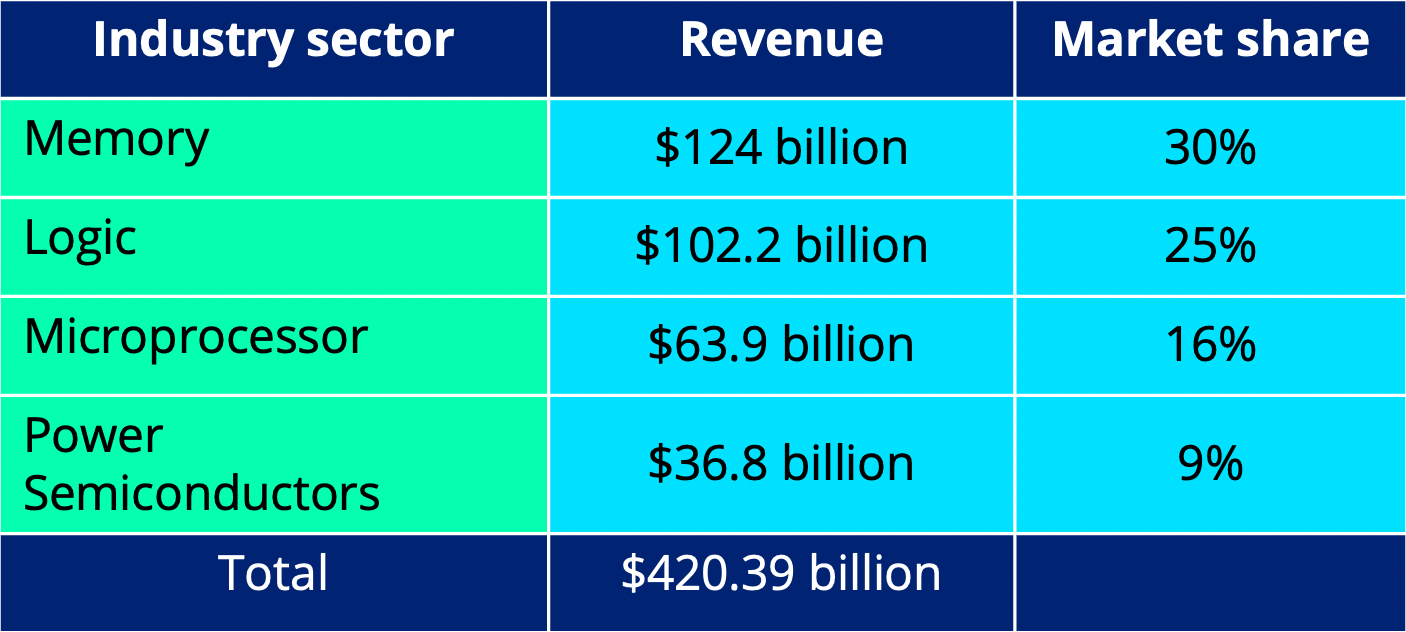

First, let’s review some data about the current market of chips. The source of this data is the Semiconductor Industry Association, which presents the following breakdown of the market.

As you can see, the market is enormous in each category. Let me focus today on Microprocessors.

There are two main types of companies in the microprocessors industry:

Manufacturers of chips Companies with factories. They can design their chips like INTEL or have a Foundry business as TSMC (Taiwan Semiconductor Company), producing chips for others.

Fabless companies

Companies without factories. They design their chips and manufacture them with Foundry business companies like TSMC. ARM and Apple and good examples.

Micros everywhere

In the last twenty years, chips have appeared in every device you can imagine, and consequently, the market has grown x5 in the last twenty years.

However, the growth has occurred unexpectedly for me.

Twenty years ago, there were more than 2000 Fabless companies. A lot of startups designed their chips and manufacturer thru some manufacturers.

Today, there are only 200 Fabless companies.

Twenty years ago, the number of manufacturers was similar to now; INTEL, Samsung, and TSMC were already there. However, their margins per chip were 30%.

Today, the margins of these companies are closer to 60%. The price went up!

Another surprise for me is the dominance of TSMC. They control 55% of the market share; they have the most advanced manufacturing technologies used by Apple or ARM. Their power is enormous; they tell their customers how much they can sell to them. They dominate because they have deep expertise in manufacturing processes. Everyone can buy machinery, but they know how to use it.

Today, Intel, Samsung, and TSMC have the most advanced manufacturing technologies and countries, as China has invested more than $100b without success. There is a geopolitical game with the chips because the USA, Korea, and Europe still have technological power over China.

Will the Power Magnetics follow a similar evolution?

After understanding the semiconductor evolution, the question of how the magnetics for power supplies market will be in 20 years blows my mind.

A lot of small manufacturers in Europe have disappeared. The giant Asiatic Yageo and Chilisin are growing in this market thru acquisitions. However, they don´t have the mastery technology to design these components.

The fabless companies of power magnetics are represented by all the power supplies companies that design their magnetics. The manufacturers are the winding houses.

The designers look the magnetics as electrical components and the manufacturers as mechanical components.

Big companies are struggling suppliers with cost reduction. However, SMEs are paying much higher prices for smaller quantities. The economics of scale aren´t balanced here because of the lack of a prominent leader in the industry.

But again, who create the technology?

Researchers are publishing models to improve the accuracy of the calculations of the current technologies.

Materials manufacturers are improving the stability of their materials.

But the true advanced designs and technologies are created secretly by private companies in sectors like telecom, automotive and military. They protect their competitive advantage through patents or industrial secrets. Topologies and magnetics represent the main differences between automotive TIER1 competitors.

There isn´t an equivalent to TSMC or ARM in our industry because the most advantageous technology is in the power supply teams of automotive companies. Some winding houses have a good understanding of the manufacturing process with resins and complex windings, but the real innovation comes from electrical and mechanical engineers working together.

Our Vision

After seven years at Frenetic and seven years doing research during my PhD, my vision have evolved.

At the beginning of 2016, I was convinced the problem was the need for more investment from the core manufacturers. Core shapes based on toroidal shapes with distributed gaps will be the best solution.

We work on proprietary materials to be printed with a 3D printer.

Then we learned about the current core materials and shapes could be exploited much better. We started drawing Frenetic Online, focusing on understanding the waveforms of each circuit to provide the best response. Then, we found the problem of the model's accuracy or calculation time of FEM software. Most calculations can get a high-accuracy prediction using advanced models from the best researchers. For the rest, we can use AI. We could solve the leakage inductance or capacitance in seconds with high precision using AI algorithm and a results database.

The result is Frenetic Online, a great simulator in terms of accuracy and speed.

But we dream bigger. Now that we know how to design and produce parts connecting factories worldwide with the most advanced Lab of magnetics and software able to provide accurate simulations. It’s time to innovate.

Our vision is to create specific technologies to get x10 improvements in particular designs and applications—for example, audio amplifiers or OBC.

These technologies will be divided into the following areas:

Manufacturing technologies

Resins and passive cooling systems

Integration of power magnetics and silicon devices

But what is more important, the innovation will come with the unification of mechanicals and electrical engineers working together.

I’m already working on it in our new Frenetic House Laboratory. I know it will take us years. TSMC needed 30 years to become an industry leader; I’m not in a rush and to be honest, I’m having a lot of fun.

A take away message..

The Custom Power Magnetics industry is evolving to be dominated by a few manufacturers; prices will increase, especially in medium-low volume products, and the number of electrical engineers is not growing, what means, we will need acceleration tools to fulfill the demand. High-Frequency magnetics are trending in the industry, but there isn´t a clear leader for the custom pieces.

The integration of magnetics with silicon devices could be a differentiator.

Key players will have differential technologies in design, but also in manufacturing.

Teams that combines Electrical and Mechanical expertise will win.

References

https://statisticsanddata.org/data/top-semiconductor-companies/

https://www.quora.com/Where-are-AMD-processors-manufactured